What are the five most important formulas in finance for company valuation? And how can you apply them to your everyday life, whether you are in the venture community or not?

1. The Time Value of Money:

Or, “a dollar today is worth more than a dollar tomorrow”.

The formula:

Present Value = Future Value / (1+r)^n, where “r” is your discount rate, and “n” is the number of periods.

Today’s inflation makes this clear:

Price of milk is increasing by 10% every year, so a gallon of milk that costs $1.00 today will cost $1.10 next year.

And $1.21 the following year. That $10 bill in your pocket buys you 10 gallons today, but only 8.2 gallons in two years!

The “r” in the formula is the discount rate at which we discount future profit.

$1 in the next period is only worth 1/(1+r) today.

And $1 in three periods is only worth 1/(1+r)^3. The further out the future cash flow, the exponentially smaller its value today.

It is also important to note that “r” takes not only inflation, but also risk into account. If your neighbor tells you they will give your $10 in two years, not only does that buy you less milk, but they may move house and never pay you.

Given the risk, you may want $5 today vs. $10 in two years!

So how can you apply time value of money to your life?

Be aware that with 10% inflation and 0% interest on your $9,000 savings account, you are $900 poorer at the end of the year. Congratulations, you just paid the inflation tax!!

Invest your money (wisely) and don’t let it melt away!

2. The value of a constant growth annuity:

Or, “even an infinite cash flow has finite value”.

The formula: Present Value = Perpetual Cash Payment / (r – g)

In this formula, “g” is the constant growth rate, and “r” the discount rate from Formula #1.

The simpler version of this formula is the No Growth Perpetuity – a cash flow forever that does not grow.

That formula is: Present Value = Perpetual Cash Payment / r

If “r” is 10% and you win the lottery to receive $1,000 every year that is worth $10,000 in today’s dollars.

You can apply this formula to value mature companies quickly:

If a company will only grow 5% over the foreseeable future, and is earning $10 million in after-tax profits, and your “r” is 15%;

The company is worth $100 million today.

$10mn / (15% – 5%) => 10mn / 0.10 => 100mn

There are many implications of this formula.

i.) companies & cash flows have finite value, driven by math

ii.) growth increases the value of future cash flows

iii.) risk & inflation decrease value

iv.) predictability decreases risk

You can see why “predictable growth” is something of a home run in valuation terms!

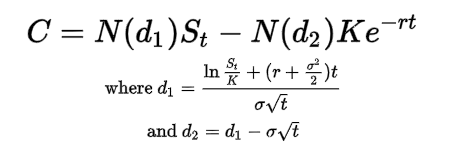

3. The Black-Scholes formula:

Or, “options have value”.

The Black-Scholes is a bit too complex mathematically to get into here.

But the implications of Black-Scholes are simple and valuable!

The implications:

i.) Options have value; never give one for free unless you are getting something in return

ii.) Value of options increase w/ volatility & duration

In risky times, (or if you are wise enough, before the risky times come knocking at your door), secure options.

Flexibility has value as it lets you pursue more options.

Value flexibility.

4. Enterprise Value vs. Equity Value

Or, “debt is never free”.

The formula:

Equity Value = Enterprise Value – Net Debt.

The best way to think of this is in terms of your house.

Your house may be worth $300,000. But you have a $250,000 mortgage – debt to the bank.

Your equity in your house is only $50,000.

The same concept applies to a company valuation. So in a situation where a company has taken on debt, we need to think of two concepts.

Enterprise Value: The analog to the value of the house from above.

Equity Value: The analog to “equity in your house”, or what is left when the debt is paid off.

If your valuation is based on net income, this is not an issue.

100% of net income is for equity holders, & is net of debt service.

But if your valuation is based on revenue or EBITDA you need to look at how much debt there is.

And subtract it from the Enterprise Value.

Implications:

i.) Debt gets paid of first. When enterprise value goes down, equity value gets wiped out first. Be aware.

ii.) Do not confuse enterprise cash flows (revenue, EBITDA), with equity holder cash flows (Net Income)

iii.) There are things that don’t look like debt, but are

iv.) When you are referring to a company’s value, especially in private markets, know if you are talking about enterprise value or equity value.

v.) Public markets do not have this confusion: All stocks are traded based on equity value.

vi.) Take on debt judiciously

5. The Capital Asset Pricing Model (CAPM)

Or, “return expectations are driven by inflation as well as a risk premium”

The formula:

Expected Return = Risk Free Rate + Risk Premium

The Risk Free Rate is measured by a safe asset such as a short dated U.S. T-bill.

This is what investors can earn without taking risk.

In the long run, this is very correlated with inflation.

In the short term there can be lots of deviations we need not get into here.

The Risk Premium is derived from:

– The overall risk appetite in markets (equity risk premium). This can go up and down based on the macro situation.

– The systemic risk of the security (also known as Beta, it is a measure of how much risk a security contributes to a portfolio).

Implications:

i.) Higher inflation => higher risk free rate, higher “r”

ii.) Macro uncertainty => higher equity risk premium, higher “r”

iii.) A risky venture => higher Beta, higher risk premium, higher “r”

More macro risk & more inflation, is not great for venture valuations!

In summary:

Pass on inflation into your net profits if you can. Predictability of growth will reduce your investors’ “r” & increase valuation. Take on debt judiciously. We are in a new reality with valuations, get used to it, and accept it. Things will change, but only as the macro situation and the inflation outlook improves.