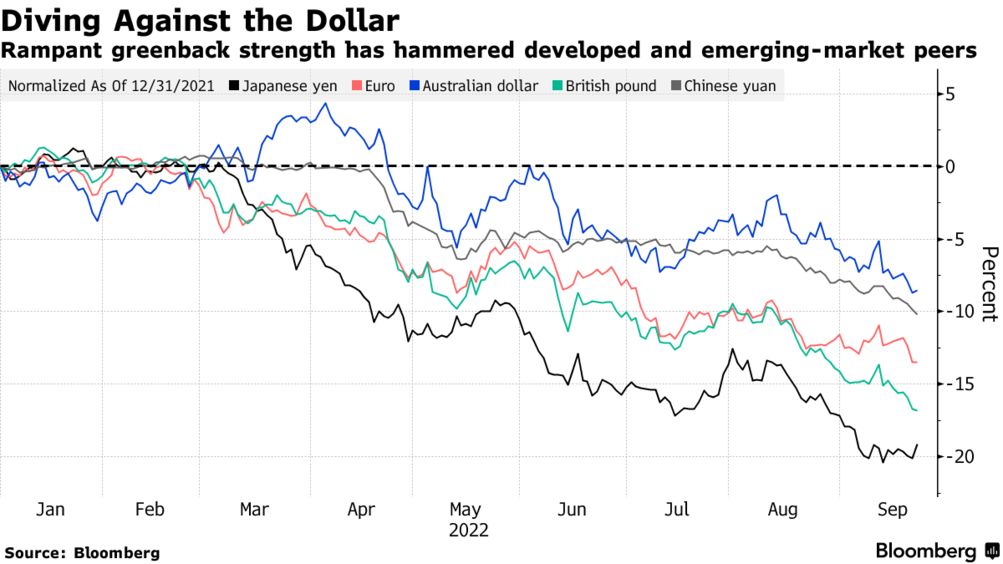

As if we need a reminder that we live in volatile times, the global currency markets gave us a bone-rattling jolt over the last week as the British pound hit a historic (or arguably hysteric) all-time low against the U.S. dollar, prompting abundant commentary and an avalanche of new memes in social media. While a lot of what happened was idiosyncratic issues related to Britain, the U.K. is certainly no island when it comes to being exposed to the vagaries of global markets.

In fact, in our last blog we had covered the precipitous drop in tech valuations and how we could make use of simple discounted cash flow formulas to estimate what a company may be worth fundamentally. After all, in a world where markets seem to be prone to changing their minds by an order of magnitude over short periods, we all need something solid to hold on to. Mathematic formulas certainly seem to be as good as any place to get some comfort.

While discounted cash flows are a big part of modern finance, as promised, there is one other big area that we had not yet covered – the realm of options and how to price them.

Stated simply, an option contract gives the holder the right to buy, sell or use an asset at a pre-determined price at some point in the future. While many people think that option contracts came into existence along with the Chicago Board Options Exchange (CBOE) on January 1st, 1973, they have existed for much longer.

In fact, the first record of financial options in history date back to the fourth century B.C. when the ancient Greek philosopher Thales of Miletus decided to take a break from the rigors of philosophy in order to profit from his prediction that the forthcoming season would bring with it a record olive harvest. Not having the funds to buy olive oil presses at scale, Thales instead gave a smaller sum of money to each press operator in Miletus, securing the right to use them during harvest season. And when his prediction came true, Thales sold the right to use these presses (for a considerable profit) to all the olive producers who were eager to convert their record harvest into oil.

Of course, the modern option contracts that were written at the CBOE in 1973 have come a long way over the ensuing millennia. More importantly, the way options are valued has evolved just as dramatically.

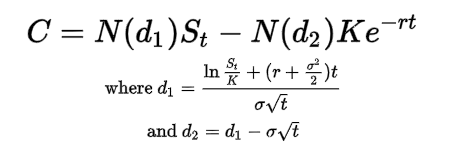

Specifically (and not entirely coincidentally), 1973 was also the year in which Robert C. Merton published his seminal paper “The Pricing of Options and Corporate Liabilities” in the Journal of Political Economy. This paper was revolutionary as it was the first to expand the mathematical understanding of a formula which had been under development by Fischer Black and Myron Scholes since 1968. Calling it the “Black-Scholes option pricing model” the formula revolutionized modern finance and provided scientific legitimacy to the CBOE and other options markets around the world, and ultimately resulting in Robert Merton and Myron Scholes receiving the Nobel Prize in Economics in 1997.

The formula itself is based on a parabolic partial differential equation, and can look quite intimidating to those not well versed in post graduate levels of math and physics.

However, there are several practical implications of options pricing that are relevant for the start-up and early stage investing world.

First and foremost, as Black-Scholes tells us, options have value. Hence, if you are giving somebody an option, you are giving something of value and vice versa. As an early-stage founder, if you can incorporate free options into your business, you should always look to do so. These can take the form of distribution agreements, supply contracts, or even a built-in feature to take your product in a certain new direction in the future. So keep your options open whenever it is practical to do so. Conversely, when you are asked to give somebody an option, for example a bank asking to do a proof of concept with an option to extend the contract, know that you are giving away something of value.

This actually brings us to the world of real options, which is the right to make (or else abandon) some choice or course of action that is available to the founders and managers of a startup. There is a whole host of literature that is focused on using real options to value startups since using a discounted cash flow can be so tricky given how uncertain the future can be. In this view of the world, the value of a startup goes up in proportion to the number of options it has to go after big market opportunities as new information flows in.

Speaking of uncertainty, one of the key takeaways from Black-Scholes is that the higher future expected volatility is, the more valuable an option becomes. So in volatile environments, and the startup world would certainly qualify as such, options become even more valuable. Similarly, the longer a period the option is valid for, the more valuable it becomes.

There are also implications here for your organizational design and the kind of people you recruit to your company in the early days. The more flexible your organization is, the more it would be capable of rapidly persecuting different courses of action, thus taking advantage of various embedded real options.

Hence, for an early-stage company, having a culture and organizational structure that enables rapidly tacking or jibing as the business environment changes is not just valuable – it can mean the difference between winning or losing in a volatile world.