In my last blog, I mentioned the slightly disquieting and amusing fact that your money does not exist. People usually have one of two reactions to this statement. If they are an economist or a student of the modern banking system, they say “Yes, so what?” whereas if they are part of the remaining of 99.9% of the population the reaction is usually a mixture of “What have you been smoking?” and general disbelief.

The easiest way to prove the point is to use a simple example, and here it goes. To illustrate that this is not directly related to the digitalization of money which is a separate issue (i.e. paper vs. digital money), let’s consider a bank in an economy that only uses paper banknotes.

In this paper money based economy, imagine Customer #1, who now goes to a bank to deposit her $1,000 in banknotes. The bank happily accepts her money and gives her a little paper ledger that shows an account balance of $1,000 (effectively the bank now owes her $1,000). Our trusting Customer #1 may be thinking of her banknotes living a comfortable existence deep down in a secure bank vault, the equivalent of money heaven.

However, in reality, the bank is much more than a simple safe or a vault for locking up banknotes. The bank needs to make money as well, and to do so, it takes the vast portion (let’s use 90% for illustrative purposes) of Customer #1’s money and lends it out to Customer #2.

Now, Customer #2, who we can imagine to be a bread maker, takes the $900 the bank lent him, and sets out to use his $900 to buy himself a new bread oven for his soon to be opened bakery. Hence, Customer #2 goes to Customer #3 (who happens to be a bread oven maker) and gives him the $900 in exchange for the latest model bread oven.

Customer #3 who sells bread ovens has no interest in putting his money under his pillow either. Hence, he takes his new $900 and goes back to the bank and deposits it. The bank gladly accepts the money and gives Customer #3 another paper ledger that shows his account balance with the $900 on it (so the bank now owes him $900).

Let’s take a little break here and consider how the situation and all the various ledgers look. The bank only has $1,000 in its safe, but Customer #1 has a ledger that tells her the bank owes her $1,000 while Customer #3 has a ledger that tells him the banks owes him $900. If they both were to go to the bank to withdraw all their funds (a total of $1,900) the bank would have to tell them that all the money is not there.

So what gives – where is the money? Of course, the short answer is that the bank has $1,000 in cash, while Customer #2 (the bread baker who took out a loan), owes the bank an additional $900 that he will pay back with the profits from his soon to be opened bakery shop.

Of course it does not stop there. Once Customer #3 (the guy who sold the bread maker the oven) puts his $900 into the bank, the bank once again lends out a big portion (let’s again use 90% as an example). Hence the bank takes $810 and lends it out to Customer #4 who uses the money to buy bricks to build herself a new house, etc.

I’ll spare you the math and the repetitive examples, but when all is said and done, the bank is left with $1,000 in capital (cash in the vault), while the sum total of all the money in the customer’s ledgers is actually $10,000. In other words, Customer #1, Customer #2, Customer #3, etc. all collectively think they have $10,000 of cash in the bank, whereas the bank in reality only has $1,000. Hence, the bank has created $9,000 of “imaginary cash” that does not exist, except as a collective belief. (My math here is only directionally correct, as the real-life computations are complicated by centuries of banking and accounting regulations and customs.)

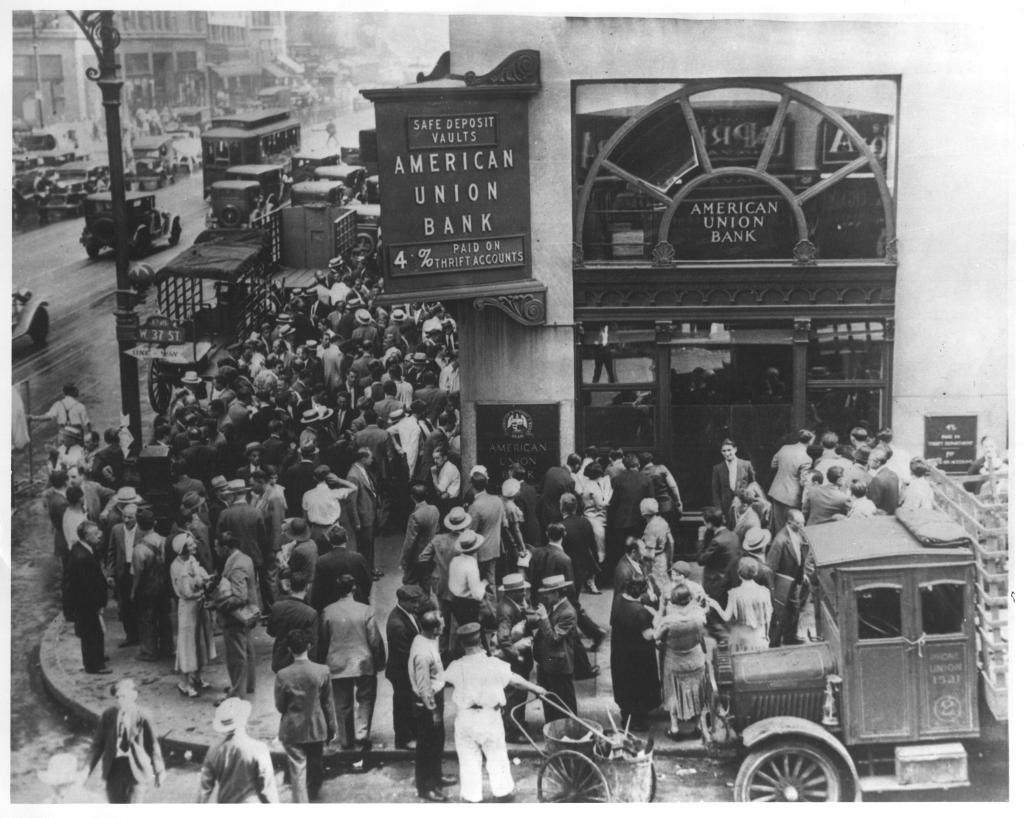

One implication of this this is that banks are vulnerable to “bank runs” that occur when people for whatever reason believe a bank is no longer trustworthy (this kind of panic can occur for any reason but usually involve rumors about the bank’s viability). This creates a self-reinforcing herd behavior where all the customers go to the bank to get their money out simultaneously. As even the healthiest of banks would not actually have all this money as we saw above, long ques form up in front of the bank which make the bank run worse, resulting in a vicious cycle that ends with the bank going bust, and the depositors losing their money.

It is for this reason that government support and the associated regulation is crucial for banks. To prevent bank runs (which otherwise would occur quite regularly), the government steps in and informs everybody that they guarantee everybody’s money up to a certain amount (the money still does not exist by the way, but the government has the power to print new money if push came to shove – this of course would create inflation but that is a whole other story). But at least the government guarantee inspires confidence and makes bank runs less likely.

So what is the relevance of all this for entrepreneurs and operators in the fintech space? One big implication, especially for those longing to one day become regulated banks, is to realize that they cannot become one without accepting the protective embrace of their respective governments and bank regulators. And that protective embrace can easily turn into a smoldering bear hug if the regulators think the bank is not being run as it should be. Hence, while becoming a bank may sound tempting, know that it comes with the full weight of history and banking regulation behind it.

After all, everything, even creating imaginary money, comes at a cost.