If capitalism were a religion, it would not be too far-fetched to think of banks as its temples, with the likes of Jamie Dimon, Ben Bernanke and Christine Lagarde the high priests and priestesses that guide the masses and interpret the will of the gods to deliver humanity peace and prosperity.

Thankfully, at least for now, nobody is making us go to banks on Sunday (except perhaps if you are an investment banking analyst working on Wall Street). However, banks still play a crucial role in our lives (whether we know it or not), and this makes it somewhat surprising that the average person doesn’t really have a good conception of how a bank actually works. One good example of this is that most people are blissfully unaware of the fact that the money they think the bank is safely keeping on their behalf in fact does not actually exist (more on that slightly disquieting but also amusing fact in my next blog).

Hence it is useful to provide a simple framework of how to think of a bank, and then use that to put the recent decade into context.

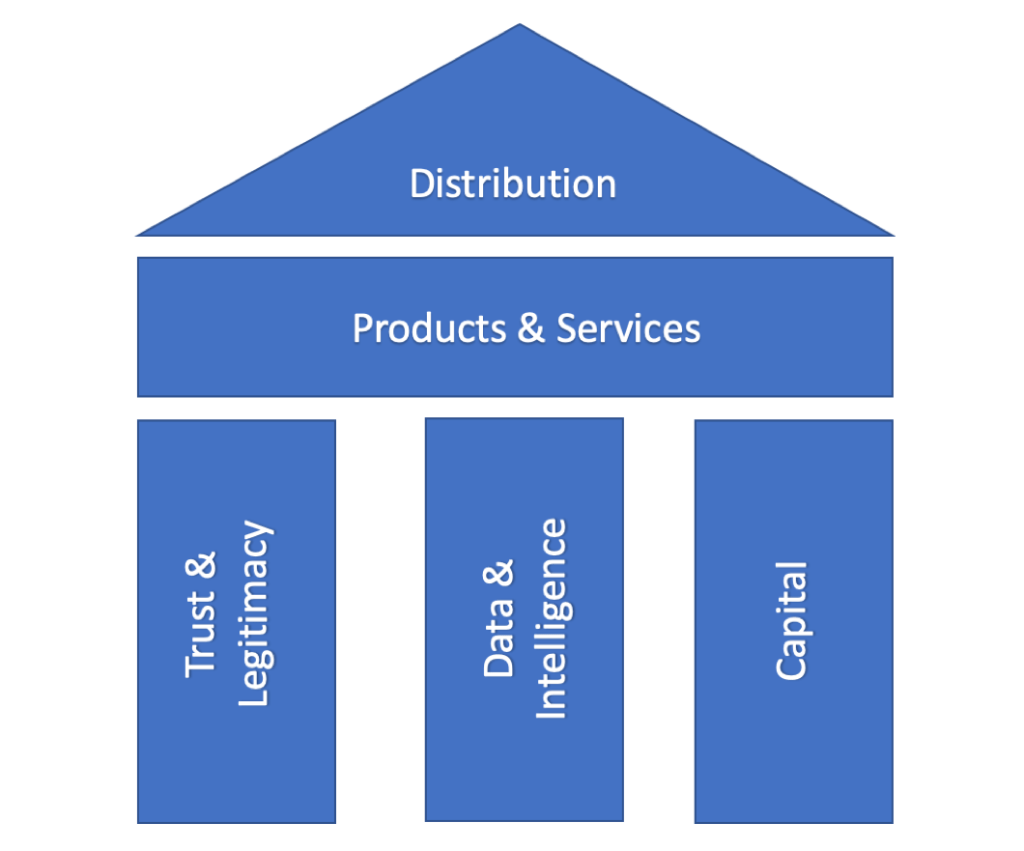

In its simplest form, banks exist on top of three fundamental foundations: trust and legitimacy, data and intelligence, and capital. Trust and legitimacy consists of the bank’s brand and public image (a bank must look secure and trustworthy, hence all the fancy suits and imposing buildings), and all its regulatory licenses. Data and intelligence used to be comprised of the bank’s employees and customer records, but in today’s world are rapidly being complemented (and sometimes replaced) by databases and algorithms. Finally, capital consists of all the funds that the bank is entrusted with from its customers, depositors and investors.

On top of these three foundations, banks build their products and services which they channel to their customers via a distribution network.

When we look at banks through this lens, we can easily see how fundamentally disruptive the events of the last decade and the crisis of 2008 has been for banks.

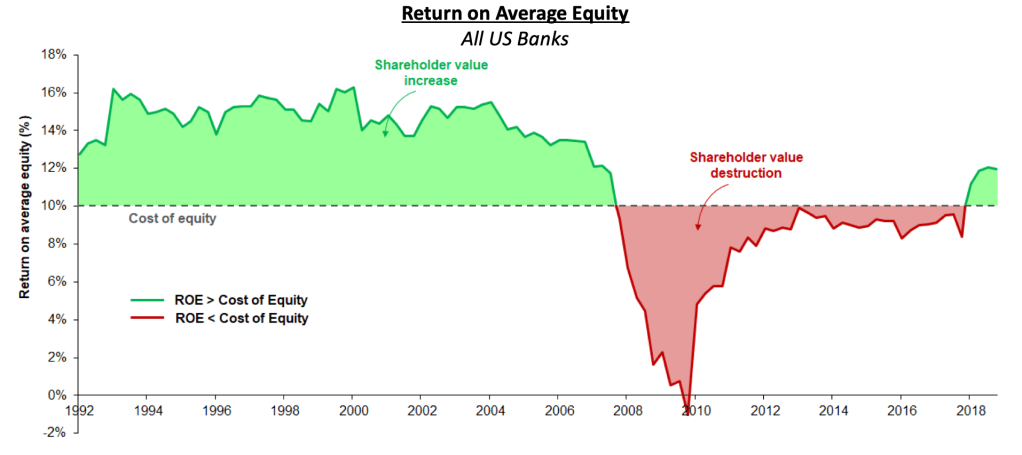

Let’s first consider the pillar of trust and legitimacy. With the onset of the 2008 financial crisis the trust and legitimacy pillar of the bank took a devastating one-two combo in the form of the trust and public image of banks being eroded severely as average citizens were being evicted from their homes, while the regulators also stepped in with new and restrictive regulations such as Dodd-Frank, not to mention multi-billion dollar fines.

As the pillar of trust and legitimacy was being shaken, there were meanwhile hitherto unprecedent changes taking place on the data & intelligence front. While in the past banks had relied on experienced loan officers and customer files with relatively straightforward data to make decisions, machines were increasingly stepping into the equation with powerful computers and complex algorithms creating an entirely new sort of decision science. And it was clearly not easy for banks to attract and nurture the kind of specialized talent needed to build those algorithms, especially given how scalable those technologies could be, and consequently how easy it could be to get funding from Silicon Valley for the top entrepreneurs and technologists.

Finally, the capital pillar came under attack from multiple directions: regulatory fines, higher capital requirements, more stringent KYC (“Know Your Customer”) requirements that resulted in a ballooning back office headcount, not to mention big losses from loans underwritten prior to the financial crises all exposed considerable cracks in capital foundation of the mighty banks.

While this all sounds bad enough in its own right, 2008 also saw the advent of a development that would add to the malaise: the invention of the iPhone by Steve Jobs and the friendly folks at Apple. So while the big banking houses were having all three pillars of their core foundations shaken, the invention of the iPhone and mobile distribution saw the roof starting to leak as well. Whereas banks had relied mostly on their vast branch networks to distribute their products and services, the iPhone enabled millions of consumers to start conducting commerce on the go, all from the palm of their hand.

To illustrate the magnitude of this challenge for banks, just consider that one of the savviest and most envied tech companies of the time, Facebook, was itself caught off-guard by the advent of mobile and it took Zuckerberg & Company a year or two to fully appreciate and adapt to mobile distribution. If the folks behind the slogan “move fast and break things” took a year to get it right, just try to imagine how things looked from the perspective of a centuries old bank, in the midst of a crisis that was shaking its foundations, with regulators and media beating down its door.

It is easy to see why the decade since the financial crisis has not been kind to banks. So, what should the banks have done? Or what can they do now? Obviously, there is a lot of firefighting happening to strengthen the foundation and fix the leaking roof, and thousands of bankers around the globe are keeping busy doing exactly that at this very moment. But to get out of the predicament banks find themselves in, there is one area that should provide a silver lining.

Banks need to get back to the core of why they exist, and that is to provide products and services to their customers. Products like credit cards were invented in a world where the nuclear families of the fifties and sixties were driving their ’57 Chevy to the newly built shopping mall to buy new and exciting consumer products such as washing machines. But the world has moved on since then. New problems exist, and new products need to be invented to solve these problems. Banks would be the obvious players to invent these products, and if they want to thrive in the aftermath of the perfect storm of 2008, this is undoubtedly what they should focus on.

The other risk is that, if banks do not create these products, somebody else will. Looking at some of the most exciting new companies in London, one can see new products being developed at a formidable speed. Income streaming (helping workers access their earned wages real-time, and thus avoiding predatory lenders – e.g. Wagestream), income sharing agreements (enabling people to borrow for school or vocational training, and only pay back if they get a bigger salary and better job which incentivizes universities to offer more relevant and employment-friendly degrees), companies that give consumers power over their data while enabling them to monetize this data (e.g. Fidel API), and companies that solve the problems faced by the elderly in a world where many people may spend more time in retirement than working (e.g. Rest Less) are just some examples.

In summary, the conclusion is simple: innovate, or find yourself relegated to history. Now is the perfect time!

2 thoughts on “Dissecting a Bank and the Ghost of 2008”